Imagine you run a small fashion boutique online. Shoppers love your products, but many hesitate at checkout when they see the total price. Add a Buy Now, Pay Later (BNPL) button, and suddenly the barrier shrinks, that same customer can split their payment, feel more confident, and complete the purchase.

This is not just a theory. Analysts project BNPL transactions worldwide to reach USD 560.1 billion in 2025, growing at 13.7% year over year (Fintech Futures). In the US, adoption is climbing across every age group: 47.4% of BNPL users are projected to be Gen Z and 40.6% Millennials (Scoop Market)

For small and medium-sized eCommerce stores, BNPL is no longer a trend. It is a lever you can pull to drive more sales, higher order values, and loyal repeat buyers.

The BNPL Market in 2025

BNPL is expanding at record speed. Reports show:

- The global BNPL market will reach USD 560.1 billion in 2025, with a long-term CAGR of about 10.2% through 2030 (Fintech Futures).

- Regional volumes: Asia–Pacific is projected to account for USD 211.7 billion, Europe USD 191.3 billion, and the US USD 122.26 billion by 2025 (Coinlaw).

Demographics: In the US, Gen Z and Millennials together will make up nearly 90% of BNPL users (47.4% and 40.6%, respectively) (Scoop Market).

The message is clear. BNPL is not a niche tool anymore. It is becoming a default expectation for online payments.

Why BNPL Works So Well for SMEs

Customers often abandon carts because the full upfront cost feels heavy. BNPL lightens that load. Here’s why it matters:

- Bigger baskets: Merchants using Shop Pay Installments (Shopify’s BNPL solution) see up to a 50% increase in average order value (AOV) and 28% fewer abandoned carts (Shopify). Separately, Klarna reports a 23% increase in AOV for merchants offering its service.( Shopify)

- Fewer abandoned carts: BNPL reduces cart abandonment by around 10% (Convertcart, 2025).

- Reaching new customers: BNPL appeals to shoppers who avoid credit cards or who prefer more flexible installment options (US Chamber of Commerce, 2025).

For SMEs competing with large retailers, BNPL can level the playing field. Choosing the best eCommerce platforms in 2025 alongside BNPL support ensures your store is built on systems designed for conversions.

BNPL Shopper Behavior Insights

Beyond increasing average order value and reducing cart abandonment, BNPL also influences customer behavior:

- Impulse spending on experiences: Gen Z and Millennials are 50% more likely than average to use BNPL for things like concerts, travel, and fitness gear (Numerator).

- Unplanned purchases: 36% of consumers made an impulse buy over $250 in the past three months, and about 10% used BNPL to cover it.

- Impulse spending lifted by nearly half: 49% of BNPL users admit they make more impulse purchases because it helps them manage upfront costs (PartnerCentric).

This shows that BNPL does more than help close sales. It also encourages customers to buy more frequently and explore new product categories.

What It Means for Your Store Metrics

BNPL directly impacts the numbers that matter most. But to measure success properly, you also need to know the right way to calculate Shopify metrics so you can track whether BNPL is driving sustainable growth.

- Average order value (AOV): Many merchants see a 30–50% increase in AOV when BNPL is introduced (WizzCommerce)

- Conversion rate: Providers like Klarna report 30–35% improvement in checkout conversions on average when BNPL is available (DirectToConsumer).

- Cart abandonment: BNPL can help reduce abandonment by up to 28%, as seen with Shopify’s Shop Pay Installments feature (Shopify)

How to Roll Out BNPL the Right Way

Adding BNPL should be a deliberate choice. To make it work for your store:

- Display installment options on product pages and at checkout. Klarna Checkout led to a 30% increase in conversions and 45% increase in AOV among merchants offering BNPL (embryo.com)

- Keep it clear: Customers trust transparent fees and terms. Hidden costs discourage adoption, which is why new CFPB rules require BNPL providers to issue clear disclosures, billing statements, and fast refunds (Time/CFPB).

- Pick the right partner: Leading BNPL providers include Klarna, Affirm, PayPal, and Afterpay, each with strengths in different regions. Your choice should depend on fees, integration options, and market coverage (Business Insider).

- Track and adapt: Measure whether AOV, conversion rates, and repeat purchases rise after BNPL is introduced. If your analytics do not match the uplift, guides like fix missing revenue in GA4 can help ensure you are capturing BNPL-driven sales accurately.

Choosing the Right BNPL Provider

Not all BNPL solutions are equal. The best fit depends on your region, fees, and customer base:

- Klarna: Popular in Europe and the US, known for flexible repayment options and high brand recognition (Klarna).

- Affirm: Focused on transparent, no-late-fee plans, widely integrated with Shopify and BigCommerce (Affirm).

- PayPal Pay Later: Strong trust factor, especially with repeat PayPal users worldwide (PayPal).

- Afterpay: Dominates in Australia and New Zealand, growing rapidly in North America (Afterpay).

- Simpl: Leading provider in India, tailored for SMEs and mobile-first shoppers (Simpl).

👉 Pro tip: Compare transaction fees, settlement times, and integration support before committing. The right partner can make BNPL profitable instead of costly.

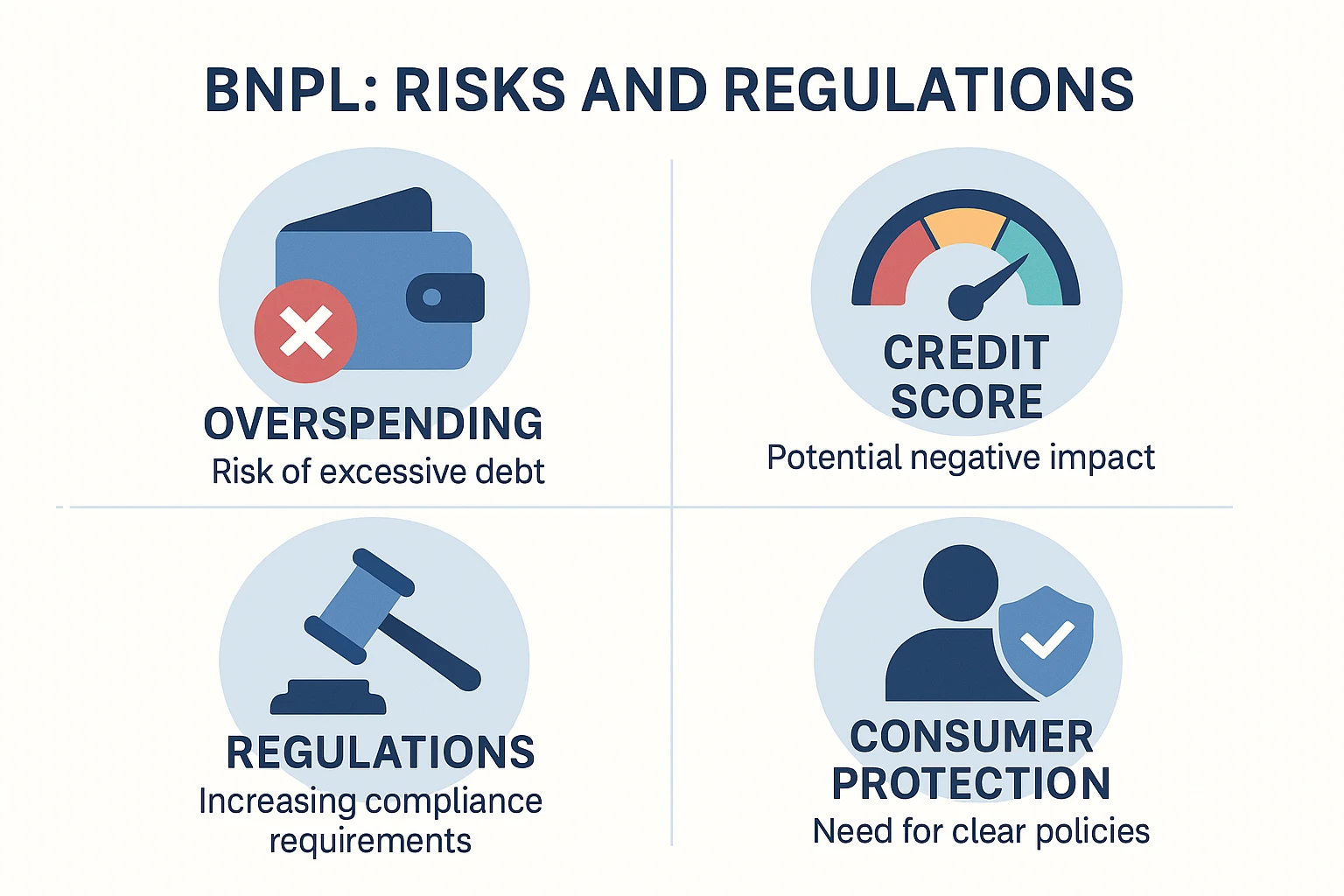

The Other Side: Risks and Regulations

BNPL comes with responsibilities:

- Overspending risks: Some shoppers may overextend and default, creating disputes.

- Credit impact: FICO has begun factoring BNPL repayment data into credit scoring, which can impact customers positively or negatively (Business Insider).

- Regulatory scrutiny: The US, UK, and India are tightening rules to treat BNPL more like credit. In the US, the CFPB now requires BNPL providers to issue clear disclosures, billing statements, and fast refunds (Time/CFPB).

- Reputation risk: Poor BNPL partners may use aggressive collection methods that harm your brand, another reason regulators are watching the industry closely (CFPB)

Partnering with reputable providers and staying ahead of regulatory changes is key.

Final Thoughts

For SME eCommerce stores, BNPL in 2025 is more than a checkout feature. It is a proven growth lever that can increase conversions, boost average order value, reduce cart abandonment, and strengthen customer loyalty.

The stores that implement BNPL thoughtfully, choosing transparent partners, staying compliant with regulations, and tracking performance will be the ones that win in a competitive eCommerce landscape.

Frequently Asked Questions

Q. Does BNPL really help SMEs increase sales?

Yes. Merchants offering BNPL report 30–50% higher AOV, 30–35% more conversions, and up to 28% fewer abandoned carts (Shopify, Klarna, Convertcart).

Q. How much is BNPL expected to grow in 2025?

The BNPL market is projected to reach USD 560.1 billion in 2025, with growth of around 13.7% year over year and projected to exceed USD 900 billion by 2030 (Fintech Futures).

Q. Can BNPL reduce cart abandonment?

Yes. Studies show BNPL can reduce cart abandonment by 10–28%, depending on the provider and how early the option is displayed (Shopify, Convertcart).

Q. What should SMEs watch out for with BNPL?

Risks include overspending, late payments, tighter regulations, and potential brand harm if you choose an unreliable provider. For example, FICO is now factoring BNPL data into credit scores, and the CFPB requires providers to issue clear disclosures and billing statements (Business Insider, Time/CFPB).